The provincial government released BC Budget 2026 in mid-February, and while budgets rarely make for light reading, this one carries some important implications for housing across British Columbia.

For homeowners, buyers, and anyone watching the real estate market closely, several of the measures introduced this year raise broader questions about affordability, housing supply, and the long-term direction of policy in our province.

A Budget Introduced in a Challenging Economic Moment

The budget arrives at a time when the provincial economy is facing uncertainty and slower growth. As expected in that environment, the government has projected a sizable deficit.

While deficits themselves are not unusual during uncertain economic cycles, economists have pointed out that the budget does not yet outline a clear path to returning the province’s debt levels to a more sustainable trajectory. Over time, rising debt-service costs can reduce the government’s flexibility — limiting its ability to provide tax relief or fund new initiatives.

For those of us who work closely with housing every day, the bigger question is how policy decisions today shape the future supply of homes across the province.

The Supply Question: A Key Concern

One of the central challenges in British Columbia’s housing market remains housing supply. Population growth continues, while new home construction has already begun to slow in some areas due to rising costs and economic uncertainty.

The concern expressed by industry economists is that several measures introduced in the budget may further increase the cost of building new homes — at a time when encouraging development is widely viewed as critical to improving long-term affordability.

According to BC Real Estate Association Chief Economist Brendon Ogmundson:

“There is unfortunately not a lot to like from either a macroeconomic or housing perspective in this budget… doing so on the back of an already struggling housing sector will ultimately prove to be self-defeating.”

Key Measures That Affect Real Estate

Several policy changes introduced in the budget directly affect those who own property, develop housing, or invest in residential real estate.

1. Higher Additional School Tax on Higher-Value Homes

Beginning in 2027, the province will increase the Additional School Tax applied to residential properties assessed above $3 million.

The new rates will be:

• 0.3% (up from 0.2%) on assessed value between $3M–$4M

• 0.6% (up from 0.4%) on assessed value above $4M

This tax applies to most residential property types including detached homes, townhomes, condominiums, and vacant residential land. For mixed-use buildings, it only applies to the residential portion of the assessed value.

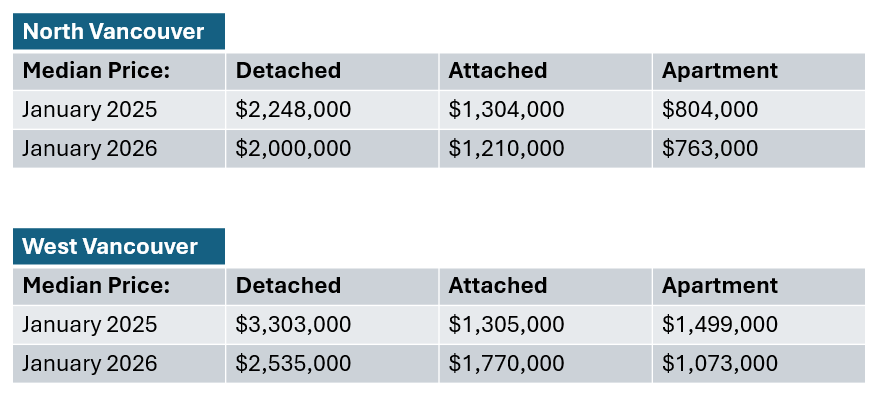

On the North Shore — where property values frequently cross the $3M threshold — this change is likely to affect a meaningful number of homeowners over time.

2. Speculation and Vacancy Tax Increase

The Speculation and Vacancy Tax will also increase beginning in 2027.

For foreign owners and untaxed worldwide earners, the tax rate will rise from 3% to 4% on the assessed value of the property.

The intent of the tax is to encourage homes to be occupied rather than left vacant. However, some economists argue that higher taxes on foreign ownership may also discourage investment capital that could otherwise support new housing construction.

3. Rising Development Costs

Other measures within the budget — including changes affecting taxation on development land and the application of provincial sales tax to certain professional services related to housing — may increase what developers refer to as “soft costs”.

Those costs are typically passed along within the final price of new homes.

In practical terms, that means policies intended to improve affordability can sometimes have the opposite effect if they increase the cost of building housing in the first place.

Why This Matters for the Market

Housing markets are influenced by many forces — interest rates, population growth, economic conditions, and policy decisions.

While the immediate impact of the 2026 budget will likely be modest, policies affecting development costs and investment can shape the housing landscape over the coming years.

In a province where demand for housing remains strong, many economists believe the long-term solution lies in increasing the supply of new homes across all price ranges.

Our Perspective

From what we are seeing on the ground here on the North Shore, the spring market is already beginning to take shape.

Buyers remain active, inventory is gradually increasing, and well-priced homes are continuing to attract strong interest. Policy changes like those introduced in this budget tend to influence the market gradually rather than overnight.

What matters most for homeowners and buyers is understanding the broader direction of the market — and how changes like these may affect long-term planning.

As always, if you have questions about how new policies may affect your home, your property taxes, or the broader market, we are always happy to help you make sense of it.

No pressure — simply here as a resource whenever you need it.